The Secret Power of VA Financing

$ave

Thousands!!

Learn The Facts About VA Financing

- How you can buy a home with no down payment!

- How to pay no closing costs!

- How to get cash back when you close!

- How to make no monthly payment for 30 days!

VA Loans—Good Deal for Veterans

More than 29 million veterans and service personnel are eligible for VA financing.

Many who have already used their loan eligibility may find it possible to buy again with VA financing by using remaining or restored loan entitlement.

As you begin learning about the VA loan process, you will realize how little "red tape" is actually involved. Other than the requirement for a veteran’s certificate of eligibility and VA-assigned appraisal, the application process is not much different than other mortgage loans. Often VA loans can be made without down payment and frequently offer lower interest rates than conventional loans.

A Good Deal!!

- No down payment in most cases.

- Loan maximum may be 100% of VA-established value (loans generally may not exceed $359,650).

- No monthly mortgage insurance premium to pay.

- Limitation on buyer’s closing costs.

- Appraisal showing property value.

- 30-year loans with choice of repayment plans:

Traditional fixed payment

Graduated Payment Mortgage (GPM) - Right to repay loan without penalty.

Who Qualifies for a VA Loan?

Veterans on active duty service (not dishonorable) of at least 90 days’ service (unless discharged early for service-connected disability) during:

- WW II (September 16, 1940, to July 25, 1947)

- Korean conflict (June 27, 1950, to January 31, 1955)

- Vietnam era (August 5, 1964, to May 7, 1975)

Peacetime veterans and active duty military personnel with more than 180 days’ active service can also qualify. Veterans of enlisted service which began after September 7, 1980, or officers with service beginning after October 16 1981, must (in most cases) have served at least 2 years.

Honorably discharged reservists and National Guard members involved in the Persian Gulf Conflict who were activated on or after August 2, 1990, and served at least 90 days are eligible.

Applicants must have a good credit rating, have an income sufficient to support mortgage payments, and agree to live on the property.

To obtain a VA certificate of eligibility, complete VA Form 26–1880, Request for Determination of Eligibility and Available Loan Guaranty Entitlement, and forward with supporting documents to your VA regional office. Your unit administrative officer will assist you.

Uses for VA Loan:

- Buy a home, including townhouse or condominium unit in a

- VA-approved project or manufactured home and/or lot.

- Build a home.

- Purchase and improve a home, simultaneously.

- Finance some home improvements (VA or lender will furnish details).

- Refinance.

A Case Study - A Case Study to Help You Understand the Benefits of a Veterans Administration (VA) Loan.

Chuck and Sonja thought renting a home in the Washington, D.C., area was their most affordable option. They had previously lived on the military base or rented an apartment. But with two children and a dog, a home with a yard became a priority. They were shocked to learn that Chuck's Staff Sergeant (E-6) housing allowance couldn’t come close to covering the rent on the most basic home.

When they were first offered the option of owning their own home, their initial response was, "No way, we can't afford it!" Then they learned The Secret Power of VA Financing.

Myth: We can't come up with the down payment.

Truth: VA financing does not require a down payment for homes priced under $359,650.

Myth: We can't afford the closing costs.

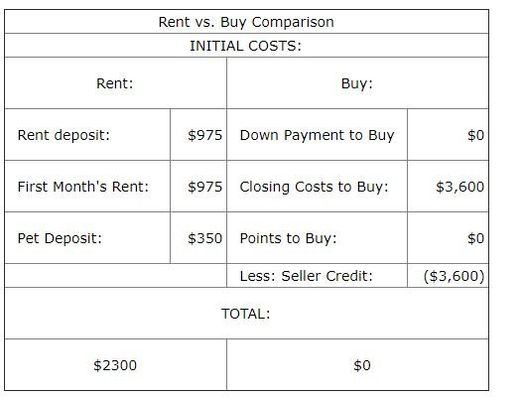

Truth: Closing costs are roughly 3 percent of the purchase price. With skillful negotiations, we were able to have the seller pay the closing costs. Chuck and Sonja moved in with no money out of their pocket!

Myth: We can't afford points on the loan.

Truth: Discount points are lender fees that may be paid up front for a reduced interest rate over the life of the loan. Under current market conditions, most buyers don’t need to pay points.

Solution: Chuck and Sonja purchased a beautiful home and paid no down payment and no closing costs. The deposit they posted with the offer to purchase was refunded the day they occupied their new home. Their first payment was not due until 30 days after they moved in. And, the extra month of housing allowance paid for Sonja's new curtains! PS: The children and the dog love the yard!

Chuck and Sonja saved $2,300 on INITIAL COSTS!!

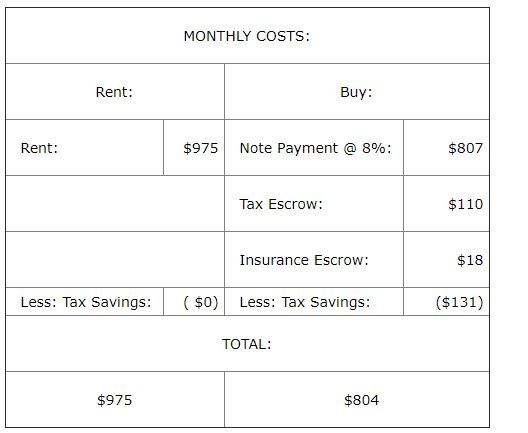

Chuck and Sonja saved $171 per MONTH, $2,052 per year!!

Requirements for Loan Approval

To obtain a VA loan, the law requires that:

- The applicant must be an eligible veteran who has available entitlement.

- The loan must be for an eligible purpose.

- The veteran must occupy or intend to occupy the property as a home within a reasonable period of time after closing the loan.

- The veteran must be a satisfactory credit risk.

- The income of the veteran and spouse, if any, must be shown to be stable and sufficient to meet the mortgage payments, cover the costs of owning a home, take care of other obligations and expenses, and have enough left over for family support.

We will be able to discuss specific income and other qualifying requirements with you.

Costs of Obtaining a VA Loan

Funding Fee—A basic funding fee of 1.5% must be paid to VA by all but certain exempt veterans. A down payment of 5% or more will reduce the fee to 1¼% and a 10% down payment reduces it to 1%.

The funding fees differ for reservists and National Guard individuals, for refinancing, and for second entitlement.

Closing Costs—Reasonable closing costs are charged by the lender and may not be a part of the loan amount. These are paid by the purchaser, seller, or shared as has been agreed in the purchase agreement. These costs would include VA appraisal, credit report, loan origination fee, discount points, title search and title insurance, state and local taxes, and survey.

No commissions, brokerage fees, or buyer broker fees may be charged to the veteran buyer.

Restoration of Entitlement

Veterans can have previously-used entitlement "restored" to purchase another home with a VA loan if:

- The property purchased with the prior VA loan has been sold and the loan paid in full, or

- A qualified veteran-transferee (buyer) agrees to assume the VA loan and substitute his or her entitlement for the same amount of entitlement originally used by the veteran seller. Remaining entitlement and restoration of entitlement can be requested through the nearest VA office by completing VA Form 26–1880.

- The entitlement may also be restored one time only if the veteran has repaid the prior VA loan in full but has not disposed of the property purchased with the prior VA loan.

VA-Guaranteed Loan

VA loans are made by a lender, such as a mortgage company. VA’s guaranty on the loan protects the lender against loss if the payments are not made and is intended to encourage lenders to offer veterans loans with more favorable terms. The amount of guaranty on the loan depends on the loan amount and whether the veteran used some entitlement previously. With the current maximum guaranty, a veteran who hasn’t previously used the benefit may be able to obtain a VA loan up to $359,650 depending on the borrower’s income level and the appraised value of the property. The local VA office can provide details on guaranty and entitlement amounts.

Frequently Asked Questions:

Q: Who is eligible for VA financing?

A: Any active duty member with 180 days of military service, or a separated or discharged member with 2 years prior service.

Q: How many times can I use my VA loan eligibility? I've heard that it's only good for one loan.

A: You can use your VA loan guarantee over and over again for the rest of your life. You can buy more than one home using VA financing.

You will save THOUSANDS when you learn about the secrets of VA Financing!

What You Learned about VA Loans:

- How you can buy a home with no down payment!

- Pay no closing costs!

- Get cash back when you close!

- Make no monthly payment for thirty days!